Contact us

About us

At Good Life Homes, we have a simple business approach:

"To treat all clients in the manner we would like to be treated ourselves".

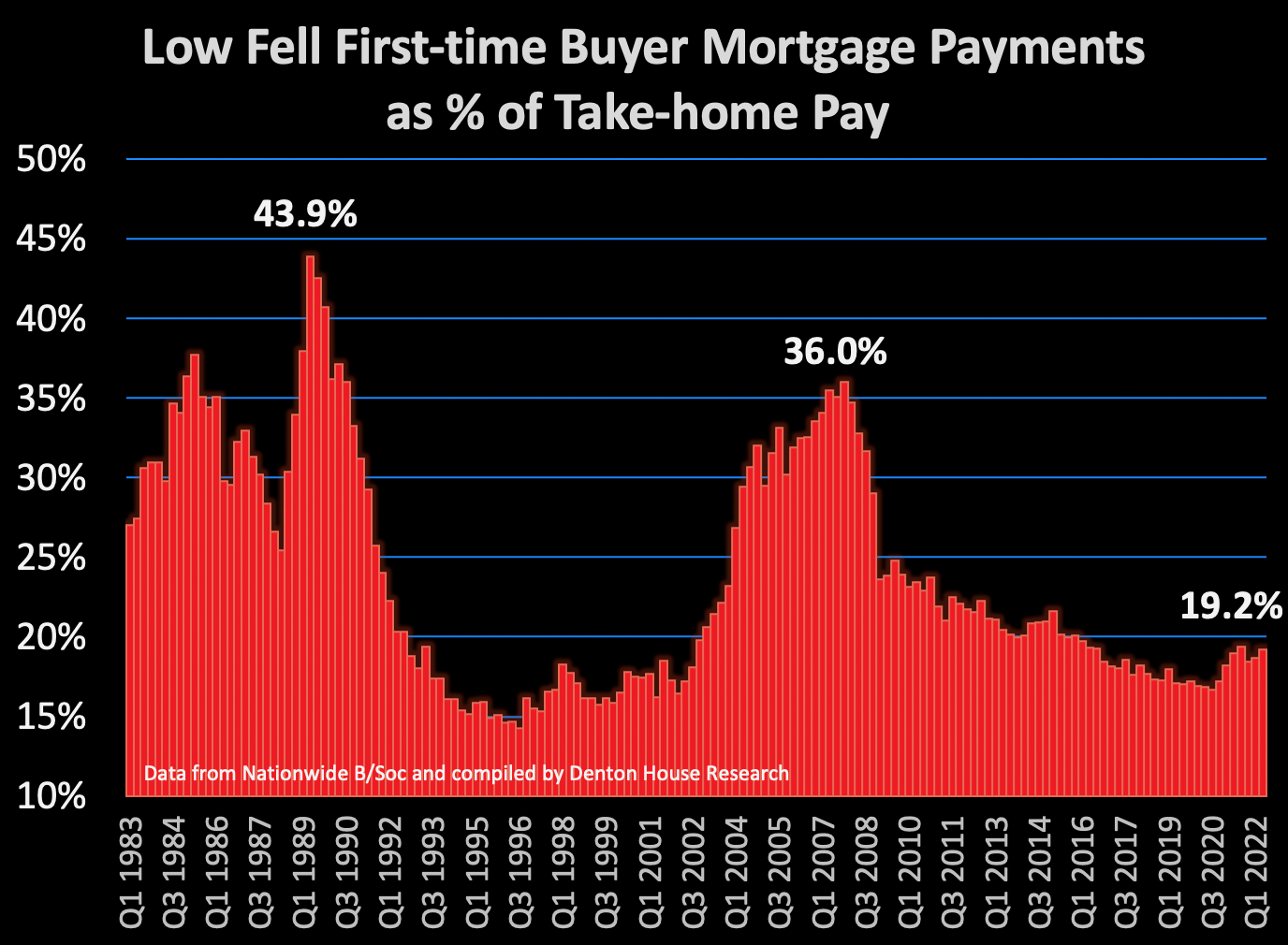

Even though the average value of a Low Fell first-time buyer property has risen by 279.2% since 1989 to £187,540 the monthly payments Low Fell first-time buyers must make on their mortgages as a proportion of their take-home pay is 56.2% less today compared to 1989.

Today, according to the Nationwide Building Society…

the average Low Fell first-time buyer only needs to pay out 19.2% of their household take-home pay on their mortgage payments, compared to 43.9% in 1989 (i.e., over a half less).

You might say 1989 was 33 years ago, a long time ago and not relevant to today. I would agree.

So next, I looked a little closer to home, and in 2007…

the average Low Fell first-time buyer had to spend 36.0% of their household income on mortgage payments (i.e., 46.5% proportionally cheaper than today).

So why do I say all these things?

Last month, the Bank of England revealed that its Financial Policy Committee would be removing their mortgage market affordability test on people taking out mortgages in August.

The test was introduced in 2014 to ensure the UK didn’t have a repeat of the 2008 Credit Crunch and particularly hit first-time buyers with what they could afford to buy.

This rule change means Low Fell property buyers could soon be able to borrow thousands of pounds more and purchase larger homes.

The decision to withdraw the affordability test certainly raised eyebrows in the press, primarily as the Bank of England has raised interest rates five times in the last six months to try and reduce rising inflation. Yet, as stated in the first part of this article, Low Fell first-time buyers are comfortably paying their mortgages compared to previous years – therefore everything should be ok with this rule change.

The old rules tested home buyers on mortgage repayments if interest rates rose to 6%/7%, yet the Bank thought that rule was too harsh.

Not all rules have been changed, as the important Bank of England ‘loan to income ratio’ stays put.

The Bank were keen to stress that the mortgage market was not going to turn into a free-for-all, as it did in the mid-2000s when the likes of Northern Rock were offering 125% mortgages, and a sixth of all UK mortgages were given without proof of income.

I believe it will have a progressive effect on the Low Fell property market.

Many Low Fell tenants who have been paying rents far more than actual mortgage payments for the same Low Fell home, but have failed affordability assessments regardless, will now be able to get on the property ladder.

The rule change should open the Low Fell property market up a little more and allow house prices to grow in Low Fell.

I advise anyone who has been refused a mortgage on affordability in the past to speak to a mortgage arranger. If you don't know of one, drop a message to me, and I will give you details of mortgage arrangers you could talk to.

Sarah Mains

Director

At Good Life Homes, we have a simple business approach:

"To treat all clients in the manner we would like to be treated ourselves".