Contact us

About us

At Good Life Homes, we have a simple business approach:

"To treat all clients in the manner we would like to be treated ourselves".

• The number of properties available to rent in Low Fell has dropped from 108 to 43 since February 2020.

• The average rent a tenant has had to pay in Low Fell has risen from £582 to £735 since February 2020.

• Many Low Fell landlords have cashed in on the post-lockdown property boom of the last two years and sold their properties to owner-occupiers - not fellow landlords.

• The supply of Low Fell rental property isn't near what is needed, which is of benefit to Low Fell landlords rather than Low Fell renters.

The Low Fell rental property shortage is currently very evident. In this article, I will investigate why there is such a significant lack of homes available for rent across Low Fell and what it means for buy-to-let investors.

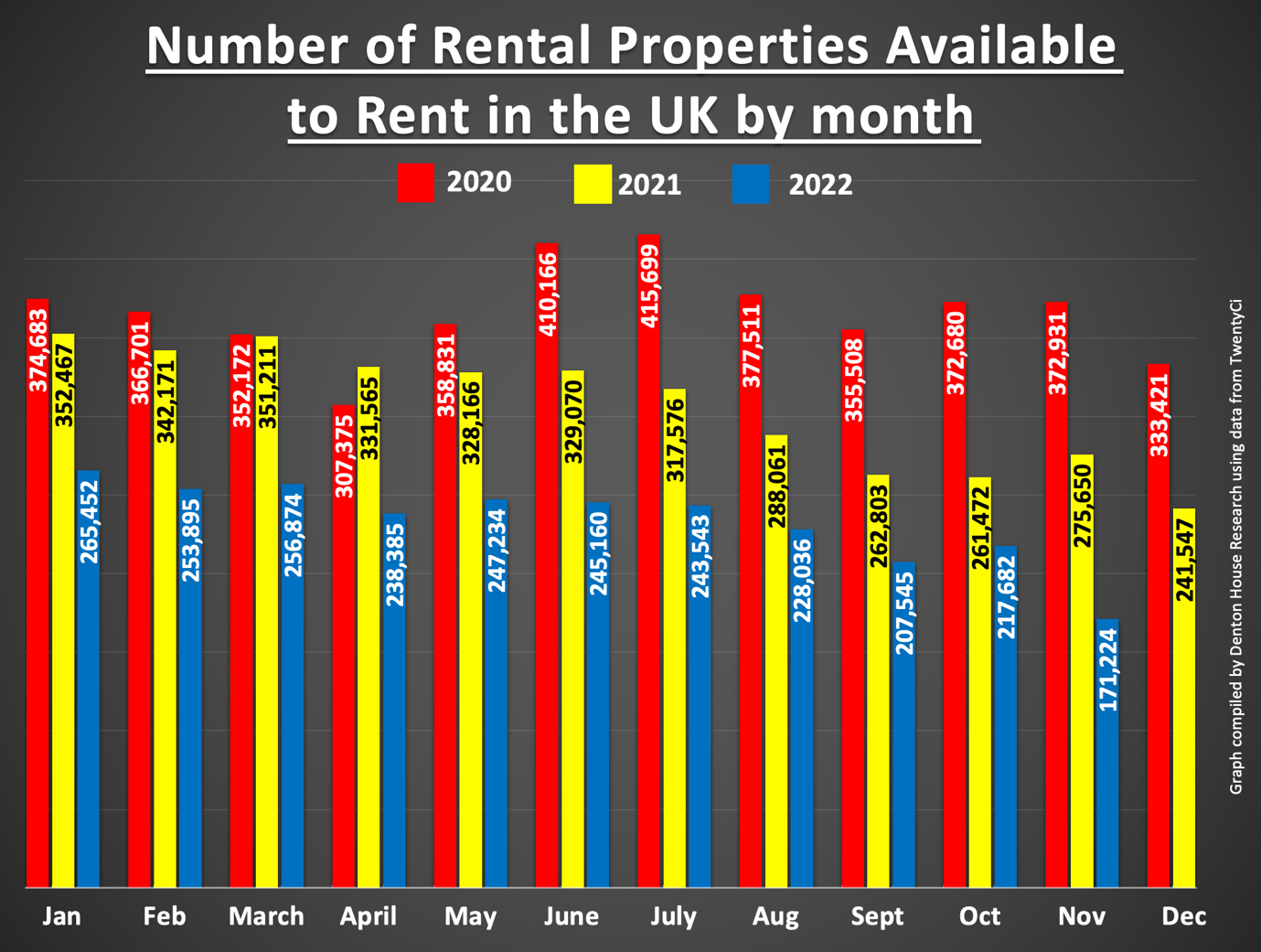

Anybody who enjoys surfing the property portals (Rightmove, Zoopla and On the Market) will have observed an emerging trend that the number of properties available to rent in Low Fell has dropped considerably in the last couple of years.

This reduction has been seen all around the UK as well. For example, on 1st November 2020, there were 372,931 properties to rent on portals. By the 1st November 2021, that had dropped to 275,650; by the 1st November 2022, that had fallen to 171,224.

That doesn't mean the number of privately rented homes in the country has dropped by over half. Fewer properties are coming onto the market to rent. I will explain why in this article.

For tenants, especially over the last 12 months, it has become progressively more challenging to find a Low Fell rental home, thus making the rent they must pay go up. This state of affairs in the property market isn’t showing an indication of getting any easier either, making for a hard time for Low Fell renters.

So, what is the reason behind the Low Fell rental property shortage, and what does this mean for existing Low Fell landlords or those potential investors considering buying a Low Fell buy-to-let property soon?

Several different components are making the perfect storm in the UK property market.

Firstly, the number of households in the UK.

The UK has not been building enough homes for the last 20 years. I appreciate that parts of Low Fell seem like one huge building site, yet as a country, we are woefully undersupplied with property to live in. This has meant house prices continue to rise due to demand.

The government have known about this issue for decades. The Barker Review of Housing Supply published in 2004 stated that the UK had experienced a long-term upward trend of 2.4% in real house prices since the mid-1970s because of a lack of house building. The report stated that 240,000 houses needed to be built each year to keep up with demand.

The average number of houses built since the mid-1970s has been around 165,000 per year, meaning the UK is short of 3,375,000 houses

(i.e., 45 years multiplied by 75,000 missing homes per year).

Several years ago, the government set a target to build 300,000 new homes each year to address this issue.

However, in 2019/20, the actual number of homes delivered stood at just 243,770. In 2020/21, the number of properties built dropped to only 216,000 new homes. In a nutshell, there are fewer available homes to buy, meaning fewer available homes to rent.

Secondly, Low Fell tenants are staying in their rental homes longer.

A Low Fell first-time buyer's average house deposit is £26,769

(the UK average deposit is £53,935).

The average rent of a Low Fell property in November 2022 is £735 per calendar month (up from £582 per calendar month in February 2020) – quite a rise!

These numbers translate into Low Fell renters not being able to pay the rent and be able to save for a deposit, or if they are saving, it is taking a lot longer to save for a deposit due to the cost-of-living crisis and higher rent costs.

Also, many Low Fell tenants have decided to stay in their existing rental homes because of the rent rises. Many landlords are less inclined to raise the rent on an existing property when they have a decent tenant who keeps the property in good condition and pays rent on time. Anecdotal evidence also suggests that rent arrears in those properties are dropping as tenants know if they don’t pay the rent, the chances are they will have trouble finding another property, and if they do, they will have to pay a lot for their next rental home.

For Low Fell landlords, this is all positive news - tenants are staying for longer in their Low Fell rental properties, arrears are lower, and void periods are less likely. When it comes to the market, there is less competition (because of the decrease in the availability of Low Fell rental properties) so this makes the investment an even better bet.

Thirdly, landlords are selling up on the back of recently increased house prices.

It would be difficult for Low Fell buy-to-let landlords to ignore the rising property prices in recent years.

The average property value in Low Fell in the summer of 2022 was 7.0% higher than in the summer of 2021.

For some Low Fell buy-to-let landlords, especially those who were classified as ‘accidental landlords’ (an accidental landlord is a landlord who never chose to become a landlord, it was just after the Credit Crunch of 2008/9, they found themselves unable to sell their property, so they temporarily let their own property out), they chose to ‘cash in’ on the higher house prices. This would have also contributed to the lack of available Low Fell homes for rent.

Yet everything isn’t all sweetness and light for Low Fell landlords.

Landlords have a few costs to consider before investing in buy-to-let, including everything from regular refurbishment costs, buildings insurance, letting agents’ fees, income tax, and, not forgetting, stamp duty.

Talking of costs, one issue some Low Fell landlords are facing is their failure to plan financially for the recent mortgage interest rate rises. Some Low Fell landlords may have become complacent to the ultra-low Bank of England base rates we have had since 2008 and, therefore, may need to sell their rental property, which, if bought by a first-time buyer, will remove another property from the Private Rented Sector.

Another hurdle to jump is the proposed new regulations requiring better energy efficiency for rental properties. It is proposed all new tenancies must have at least a minimum of a 'C’ rating for their EPC (Energy Performance Certificate) from 2025 (and 2028 for all existing tenancies).

Therefore, as a buy-to-let Low Fell landlord, it is wise to do your research to make sure the buy-to-let opportunity is correct for your rental portfolio, particularly when it comes to weathering any impending financial storms.

Landlords need to consider the returns from their

Low Fell buy-to-let investments.

Landlords can earn money from their buy-to-let investments in two ways. One is the property's capital growth, and the other is the rental return (often expressed as a yield). In 96% of buy-to-let investments, there is an inverse relationship between capital growth and yield (i.e., properties that tend to go up in value quicker will have lower yields 96% of the time – and vice versa).

Getting the best balance of yield and capital growth depends on your current and future needs from your Low Fell buy-to-let investment.

If you would like me to review your portfolio and ascertain if your existing portfolio will match your current and future needs for the investment - whether you are a client or not, feel free to drop me a line, and we can have a no-obligation chat and possibly organise a review.

What does all this mean for the Low Fell rental market?

The continued shortage of Low Fell rental properties means it will be more difficult than ever to find a Low Fell property to rent, and so rents will continue to grow.

Unlike in Scotland, England and Wales do not have rent controls, with Westminster ruling out the possibility of introducing rent control here to deal with the cost-of-living crisis.

You would think rent controls would be a no-brainer, yet economists from around the world have proved for the last 75 years that rent controls might help tenants in the short term, yet ultimately it drives landlords to sell their investments in the long term, thus reducing the stock of available properties to rent out (not great for future tenants).

Therefore, it is highly likely that Low Fell rents

will continue to rise for tenants.

Landlords who persevere with their Low Fell buy-to-let properties or become a Low Fell buy-to-let landlord are set to benefit because they have an asset in very high demand.

The housing shortage, not to mention the other issues discussed above that are affecting the supply of rental properties, is unlikely to be fixed anytime soon!

In conclusion, the Low Fell rental market is a constantly changing picture. What is known is that the supply of rental properties is far from what is needed, which can only be to the benefit of buy-to-let investors rather than of tenants renting.

I see buy-to-let as a long-term investment. Everyone reading this knows that the real value in your buy-to-let investment is playing the long game, allowing your Low Fell buy-to-let investment to grow over time. Like the crypto or stock market, getting sucked in by get-rich-quick schemes that are selling 'apparent quick wins' in property investment is very easy.

I regularly highlight the best buy-to-let deals for Low Fell landlords with all the estate agents (not just my own). You don't need to be a client of mine either to receive that information. Drop me a line or call (without any cost or obligation) if you are interested in making your first Low Fell buy-to-let investment or considering adding to your existing Low Fell portfolio.

At Good Life Homes, we have a simple business approach:

"To treat all clients in the manner we would like to be treated ourselves".