Contact us

About us

At Good Life Homes, we have a simple business approach:

"To treat all clients in the manner we would like to be treated ourselves".

A Low Fell landlord remarked to me the other day that he felt that there were more 'posher' up-market properties coming up for rent in the last six months compared to a couple of years ago.

I stated that this was the case, and it wasn't all down to the recent rental growth – it was the growth of the upmarket 'accidental landlord'.

With the Low Fell housing market showing signs of a slowdown and predictions of further house price declines, I am starting to see the return of the ‘accidental landlord’, but in a somewhat different form to what they were in 2008/9.

An ‘accidental landlord’ becomes a landlord unexpectedly or unintentionally. This often occurs when homeowners rent out their property instead of selling it due to a slowing housing market, a change in personal circumstances, or other unforeseen reasons.

While the sales market in Low Fell has experienced a period of strength in recent years, activity has started to slow down from the levels seen in 2021/2. In contrast, there has been soaring demand for Low Fell rental properties.

To give you an idea of the growth of rents.

The average rent for homes coming on the market in the Low Fell area in 2021 was £647 per month, whilst in 2023, it has been £756 per month.

Some Low Fell homeowners, fearing not achieving their desired selling price, might opt to retain ownership of their properties and instead rent them out until market conditions improve.

Back in 2008/9, this trend was particularly evident in the middle market segment.

However, in 2023, many property commentators are suggesting if ‘accidental landlords’ do start to emerge, it will be in the upper quartile property segment (i.e., the top 25% of properties by value), where many homeowners bought in the post Lockdown race for space of 2021/2.

Looking at the figures, they could be correct.

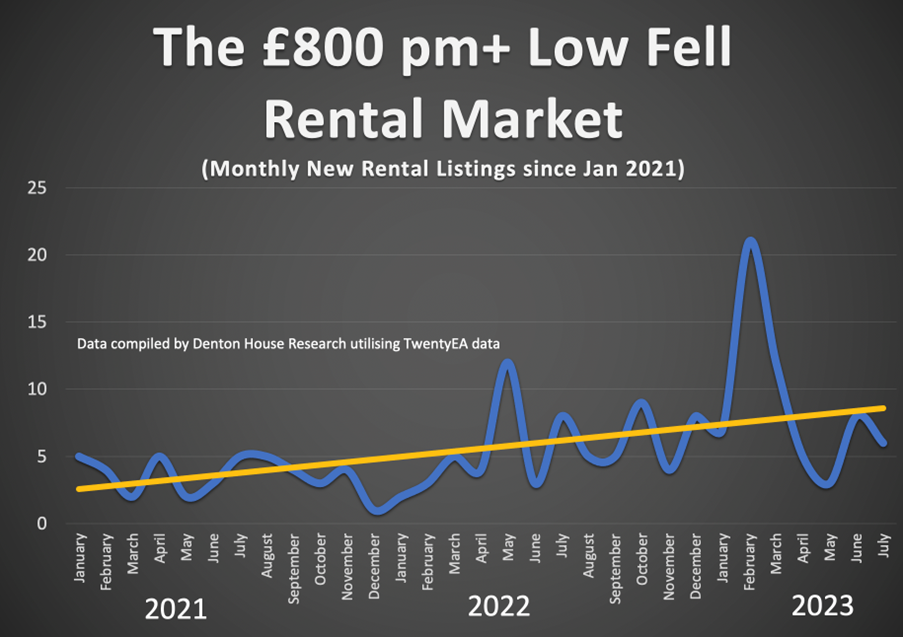

The upper quartile rental market starts in just over the £800 per month range in Low Fell.

• In the first seven months of 2021 (Jan to Jul) in the Low Fell area – an average of 4 properties a month came onto the market for rent at £800 per month or more.

• In the first seven months of 2022 (Jan to Jul) in the Low Fell area - an average of 5 properties a month came onto the market for rent at £800 per month or more.

• In the first seven months of 2023 (Jan to Jul) in the Low Fell area - an average of 9 properties a month came onto the market for rent at £800 per month or more.

(Low Fell area being NE9).

Many of these could afford to be patient in pursuit of optimal selling conditions. The rise of ‘accidental landlords’ can be attributed to various factors, such as limited property appreciation, increasing mortgage costs, and robust demand for Low Fell rentals, making renting out properties an attractive alternative.

‘Accidental landlords’ are also created through other diverse circumstances.

Irrespective of what is happening in the economy and Low Fell property market, births, deaths and marriages continue. There will always be some new couples who decide to rent out one of their properties after moving into a shared home, while others inherit properties through the passing of parents or grandparents.

The current average tenancy length of 51 months provides these new Low Fell landlords with just over four years to allow Low Fell property values to recover before re-evaluating the market. However, stepping into the role of an accidental landlord carries specific implications that homeowners need to be mindful of.

Understanding the tax implications is a crucial aspect that ‘accidental landlords’ should grasp.

Transitioning to landlord status may result in the loss of specific tax benefits, including stamp duty relief, and necessitate payment of income tax on rent. Furthermore, upon selling the Low Fell rental property, landlords may become liable for capital gains tax on the profit made from the sale, as it is no longer considered their primary residence and I implore you to take advice from an accountant.

To mitigate the impact of tax changes, some Low Fell landlords have chosen to incorporate their properties into Limited Companies. Corporate structures offer potential tax relief on mortgage costs and the opportunity to pay lower Corporation Tax rates than individual income tax rates. However, incorporating properties involves additional expenses, such as stamp duty and capital gains tax on existing properties transferred to the company.

Individual landlords with only one property may find incorporation less advantageous, but it could be a viable option for those planning to expand their buy-to-let portfolios.

Investing in property maintenance is a crucial consideration for Low Fell's 'accidental landlords'.

Well-maintained properties are more likely to retain or increase their value over time. Retrofitting properties to improve energy performance can also benefit tenants and future buyers, helping reduce utility costs and enhance overall comfort.

Accidental landlords must diligently handle this critical area: appropriately protecting tenants' deposits. Please safeguard deposits adequately to avoid significant compensation claims, with landlords potentially losing up to three times the deposit amount. To protect against such risks, landlords must ensure compliance with deposit protection schemes and provide tenants with essential documents, including Energy Performance Certificates, the Government's "How to Rent" guide, and current gas safety certificates.

Misunderstandings can inadvertently arise to renting direct to family or friends, leading to legal disputes.

Even though you know the tenant, it still could be wise to employ the services of a letting agent to establish clear terms in writing at the outset of a tenancy to avoid potential conflicts and protect the rights of both landlords and tenants. This becomes particularly relevant as the Renters Reform Bill, set to introduce significant changes to the private rental sector, including tenancy length and the process of regaining possession, is awaiting approval.

My overriding message to every Low Fell ‘accidental landlord’ is that they must be aware of the tax implications, consider incorporation a potential strategy, invest in property maintenance, protect tenants' deposits, and establish clear terms to avoid disputes. Additionally, there are over 170 pieces of regulations regarding renting your property out. Also, it's essential to stay informed about forthcoming changes in renters' rights introduced by the Renters Reform Bill.

In conclusion, with the Low Fell housing market experiencing a slowdown, I suspect an increasing number of Low Fell homeowners are considering becoming ‘accidental landlords’ by opting to rent out their properties instead of selling.

You must weigh the risks of renting your Low Fell home and the potential rewards.

I know of many stories of Low Fell homeowners who waited five or six years after the Credit Crunch to hit their ‘target price’ for their existing home, only to realise it cost them tens of thousands of pounds in costs and the price they had to pay for their new home. On the other side of the coin, I know plenty of ‘accidental landlords’ in Low Fell who used the fact that they became an ‘accidental landlord’ as an opportunity to build an impressive rental portfolio over the last 15 years.

If you are uncertain or do not possess all the facts, don't hesitate to contact me to discuss your plans. Then I can give you appropriate level-headed advice to make the right decision. By taking proactive steps and understanding the risk and rewards of being an ‘accidental landlord’ in Low Fell, you can navigate the Low Fell property market successfully, even during uncertain times in the housing market.

At Good Life Homes, we have a simple business approach:

"To treat all clients in the manner we would like to be treated ourselves".